- Economics is the study of how human make decisions in the face of scarcity. Scarcity means that wants exceed available resources.

General Quantities

- Marginal analysis is just a discretized form of the derivative.

-

Example: The marginal cost with respect to quantity is

-

Notation: For convenience, when we say, the marginal

with respect to , we mean By default, assume

is quantity We may also write this as a derivative as

.

-

The Market

- The division of labor means that the way one produces a good or service is divided into a number of tasks that different workers perform rather than one person doing al the tasks.

- Division of labor counters scarcity.

- Division of labor increases production for three reasons 1

- Specialization of workers on tasks they are well suited for, which makes them more effective.

- Specialization leads to a feedback loop where workers learn to produce more quickly and with higher quality. This also leads to innovation.

- Specialization takes advantage of economies of scale where as production increases, the average cost of production for each individual unit decreases.

- This necessitates trade because each individual specializes and must exchange their services for other needs that they are unable to produce.

- Economies are systems.

- Economics teaches you how to think, not what to think 2

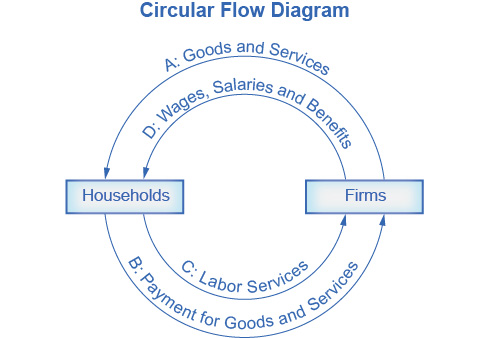

- A simple economic model is the Circular Flow Model

- Economies can be organized into different ways.

- Traditional - what you produce is what you consume. It is driven by tradition and there is little economic progress or development

- Command - economic effort is devoted to goals passed down from the government, which dictates what gets produced and what gets consumed.

- Markets - decision making is decentralized and is based on markets — institutions that bring buyers and sellers together.

- Private enterprises own and operate production based on supply and demand.

- Income is based on the ability to convert resources into something socially beneficial.

- Market-oriented economies have fewer regulations, often just enough to facilitate fair trade.

- Markets allocate goods to the people who value them the most, under the assumption that the value of the good is easily understood by all market participants.

- Underground / Black Market - often present in heavily regulated economies. This market is unregulated.

Unfiled

- Tax Incidence - the analysis of how tax burdens can be divided between consumers and producers

Topics

- Microeconomics - focuses on the actions of individual agents within the economy

- Macroeconomics - focuses on the economy as a whole.

- Money

- Computational Economics